Testimony before the U.S. Senate Energy and Natural Resources Committee

Senior Fellow Mark Mills testified before the U.S. Senate Committee on Energy and Natural Resources at a hearing entitled, “The Status and Outlook for U.S. and North American Energy and Resource Security.”

Watch the archived webcast on the committee's website

______________________

Geopolitical Implications Of The ‘Invisible’ Digital Oil Revolution

Good morning. Thank you for the opportunity to testify before this Committee. I’m a Senior Fellow at the Manhattan Institute where I focus on the policy implications at the intersection of technology and energy, and where I have advocated for years that America should have a more realistic and aggressive geopolitical energy policy posture.

I am also a Faculty Fellow at the McCormick School of Engineering at Northwestern University where my focus is on the technology and future of manufacturing. And I’m a strategic partner in a boutique venture fund dedicated to startup companies creating digital oilfield technologies. You will of course notice that my focus in all these pursuits is on the role of technology, a key force in our economy and in geopolitics which, despite popular enthusiasm for tech, is – as I will shortly explain – still under-appreciated in terms of what is about to unfold in global energy markets.

Five years ago this summer, when a different party was in charge of both the White House and Senate, I proposed in my Manhattan Institute paper entitled “Unleashing the North American Energy Colossus,” that new realities should lead policymakers to “go beyond the pursuit of energy independence” and instead “push beyond self-sufficiency to energy influence, even dominance.” I have emphasized the idea of “dominance” as a replacement for the anemic policy mindset of “energy independence” both in earlier Congressional testimony and in other Manhattan Institute policy papers nearly every year since then.

There is no dispute over the fact that food, water and energy security are critical drivers of domestic and geopolitical policies. But it’s important to note that, as the great economist, and a great friend of mine, Julian Simon once said--energy is the “master resource.” That elegant distillation of reality has far-reaching implications when it comes to geopolitics.

And in geopolitics, as in domestic politics and business in general, much of what matters gets thrashed out by means of negotiation. This is hardly news to any student or practitioner of foreign policy. And when it comes to negotiation, no one wants to come to the table as a supplicant. The preferred posture sought by everyone, everywhere and always, is to engage from a position of strength … even, ideally, one of dominance. Dominance is, by definition, having “power and influence over others.” That power can be military, with all of its attendant risks, or it can reside in the so-called soft power derived mainly from economic forces.

In his 1999 book, “A World Restored,” Henry Kissinger wrote that statecraft required the “ability to recognize the real relationship of forces.”1Kissinger, A World Restored, Oxford University Press, p. 258. [emphasis added] While aspirational goals are important, ignoring the real forces that are extant in the world is not only problematic but dangerous. And as aspirations become fanciful rather than anchored in reality, dangers rise proportionately.

When it comes to the geopolitics of energy, there are three primary forces in play.

First, petroleum today is more important to our economy, our security and geopolitics, than it has ever been in history. This is true notwithstanding popular and near universal political enthusiasm for alternative forms of energy, as well as the hundreds of billions of dollars spent in pursuing those alternatives. Consider a handful of indisputable facts.

Marked from the epoch-setting Arab oil embargo of 1973/74, global petroleum use is up 150 percent. Over 95 percent of all ground transportation is still powered by oil-burning engines. And air travel, which is completely dependent on petroleum, has increased 700 percent since then. In overall terms, transportation accounted for one-third of world oil use a half-century ago, while today it accounts for 60 percent. And oil is both the world’s biggest traded commodity and the world’s largest single source of energy.

The second primary force: For the foreseeable future, petroleum, and increasingly its hydrocarbon, natural gas, will be more not less important.

Regardless of subsidies or vigorous assertions, there are simply no prospects for reducing today’s enormous levels of oil and natural gas consumption. In fact, every credible forecast sees demand rising as global economies grow. The only debatable variable is just how big the increase in oil and natural gas demand will be over the coming couple of decades.

Not withstanding the now popular meme of peak oil demand, such a peak, when it occurs, is so far in the future as to be more relevant for purveyors of fiction rather than federal policy. And with more than one billion more automobiles expected to be added to the global fleet over the next two decades, even the most optimistic forecasts for electric cars will not lead to a world using less oil than today. Indeed, we should hope the optimists are right in order to mute the demand that’s coming. Similarly, even the most optimistic forecasts for alternative sources of electricity—whether to power cars or the information ecosystem—show that natural gas is the dominant go-to fuel for the foreseeable future.

The future is one of clearly increasing dependencies on energy imports for four of the world’s five major regions that together account for three-fourths of global GDP. China, Europe, Japan, and India are all net and rising importers of both petroleum and natural gas. Of the five major economic regions of the world, only North America is essentially energy self-sufficient and moving rapidly towards becoming a net exporter.

This rising force of energy import dependencies in all non-North American economic regions has deep geopolitical implications. Note that until very recently, the Middle East and Russia were the primary sources of new marginal supply in world energy trade.

And now the third tectonic force in the geopolitics of energy. It is a wildcard that no one expected: the role that shale technology has played in the re-emergence of the United States as both a major player, and exporter, in oil and gas markets. Shale technology is the only real energy revolution that has occurred in 50 years.

The magnitude and velocity of the shale revolution is still underappreciated. Quite simply, it was the fastest and biggest addition to world energy supply that has ever occurred in history. The only time something almost as dramatic occurred was in the decade following the 1968 opening of Saudi Arabia’s giant Ghawar oil field.

Or put in domestic terms, the increase in American energy production from shale hydrocarbons over the past decade was 2,000% greater than all the additional supply from solar and wind combined.

This revolution occurred without federal stimulus or special subsidies; nor was it the result of new “discoveries.” The location and extent of shale hydrocarbons have been known for a century. The shale revolution was the product of technology fueled by America’s capital markets combined with unique private ownership rights.

America is now not only a net exporter of natural gas – on the way to becoming a major player, perhaps “dominant” on the margin, where prices are set – but is also exporting well north of 1 million barrels a day of crude oil. That’s the highest rate of U.S. crude exports since 1958, by a factor of two, and even exceeds the exports of five of OPEC’s members. We can credit this Committee with the legislation that recognized and allowed a restoration of a legal right to export crude – something, as you know, I’ve long advocated. And we can credit President Obama for signing that legislation in late 2015. Now credit this committee and President Trump for realizing the enormous implications and pushing the idea forward still.

Importantly, world markets are impacted not just by the act of America physically exporting fuel, but also the fact that U.S. domestic production has eliminated billions of dollars of purchases of oil and gas on world markets. Both these realities triggered the collapse of global prices and kept trillions of dollars from flowing to exporting nations, mainly OPEC and Russia. No one can doubt the geopolitical ripples from such a financial disruption.

Similarly, no one doubts the subtle “soft power” impact of the massive rise in foreign direct investment into U.S. manufacturing triggered by cheap natural gas. Foreign and private domestic investments in U.S. chemical manufacturing have exceeded $160 billion in the past half decade. The full geopolitical, never mind domestic, impact of this shift is about to be realized as over 260 new chemical manufacturing projects start to come on line in the next few years.

Given these three primal forces, what comes next?

Looking to the future, the Energy Information Administration’s (EIA) “optimistic” forecast -- which assumes subsidies continue -- has solar and wind energy production growing three-fold by 2035. Meanwhile, EIA’s similar forecast for shale hydrocarbons (without subsidies of course) for the next two decades has that industry replicating its growth of the past single decade, probably a huge underestimate.

What we have already learned from the cyclical downturn in oil prices is that the technologies involved in shale production are getting better at an amazing rate. The efficacy of shale rigs – the amount of physical production per capital dollar spent – has been improving by more than 20% per year on average. Put another way; the rigs are getting roughly twice as productive every three years. No other energy technology is improving that quickly. And while, EIA data shows that the rate of improvement actually jumped during the last couple of years, the evidence now suggests that there’s much more yet to come yet.

Most forecasters today are making the same mistake they made a decade ago. They are failing to spot a revolution that is already underway. What if the shale disruption is not a one-time event in our recent history, but is only the beginning of a massive structural revolution still unfolding?

In every other corner of our economy – from retail and groceries, to housing, transportation, manufacturing and agriculture – we are everywhere reading breathless speculation about the emerging impacts of the Internet of Things, of machine learning, artificial intelligence and digital ecosystems, all enabled by cheap, ubiquitous super-computing in the Cloud.

The new and still untapped features of this next information revolution are, properly, expected to bring unprecedented power in extracting profoundly greater efficiencies, and thus economic value from every corner in the so-called “old” industrial and business activities that still comprise over 80 percent of our economy. Why should the power of algorithms combined with the Internet of Things be any less impactful in shale domains? In fact, the impact may be larger precisely because the shale industrial ecosystem is still largely untouched by the emerging digital revolution.

The category error many forecasters are making is in thinking about the new U.S. hydrocarbon industry in the same terms as the old one which was dominated by a small number of mega players each developing a small number of mega projects. In contrast, the new shale industry’s ecosystem is comprised of thousands of companies in dozens of states. It is now generating a kind of ecosystem of digital entrepreneurs -- as did Silicon Valley with other industries – in small, tech-savvy start-ups which will create the tools and solutions that will disrupt oil and gas in the same way that taxis and retail were disrupted. As I outlined in my 2015 paper titled Shale 2.0, digital disruption is coming at least as fast now in how we produce oil as in how we use it for transportation.

The emerging digital acceleration of shale fields has been noticed by Wall Street even if it has yet to be incorporated into geopolitical thinking. A new Goldman Sachs report is telegraphically titled, Shale Innovation: Brawn to Brains to Bytes. Goldman concludes that we are at the “very early stage…of the application of big data analytics and Artificial Intelligence/Machine Learning techniques to improve decision-making, equipment reliability and productivity,”

Earlier this year analysts at BofA Merrill Lynch released their report titled “The Internet of Oil.” And a new report from McKinsey calls it the “invisible revolution” … which it certainly appears to be in terms of how most energy policy is being formulated.

It’s taken time for the punditocracy to realize that the shale business more closely resembles a manufacturing industry than an “extractive” one, and it’s about to benefit from Silicon Valley-class tools as a spate of startup tech companies start chasing the big prizes associated with the world’s biggest energy market.

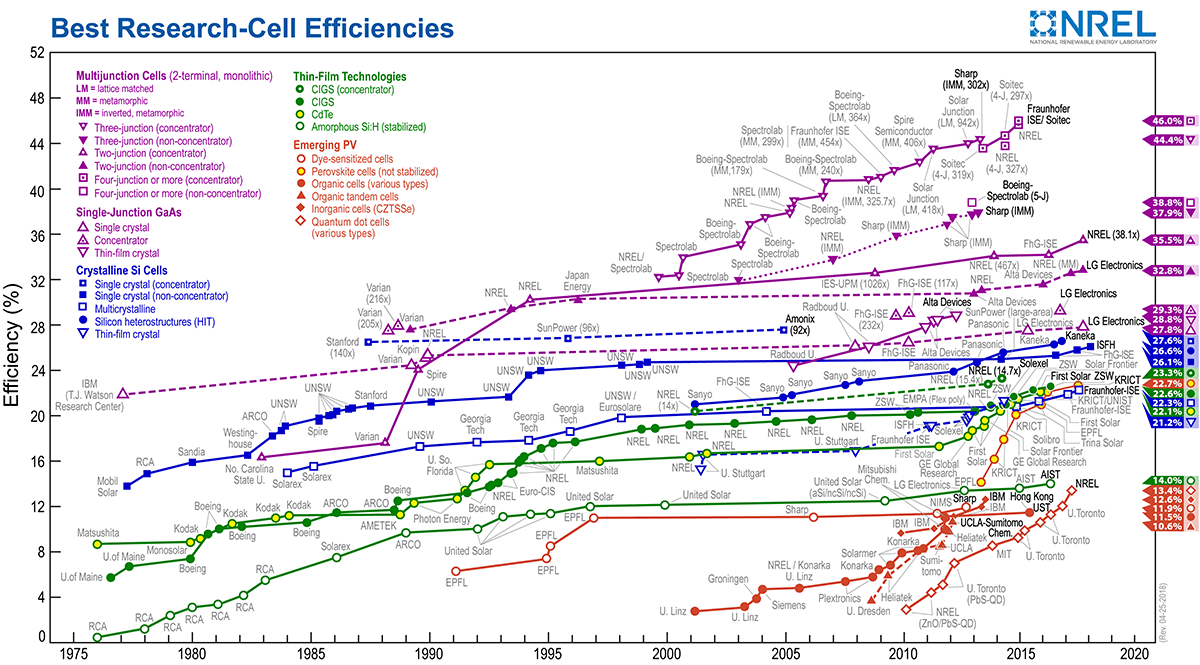

But many still believe that a future energy revolution depends on solar and wind. Of course those technologies will get far better. And of course they’re useful and important. But, as is clear from DOE’s National Renewable Energy Labs data, both wind and solar are now experiencing a declining rate of improvement as those technologies start to approach their limits in terms of what physics permits. They still improve each year, but now necessarily at a slower rate than in the past – and more relevant to our geopolitical future, at a slower rate than shale technology.

{kind=link}

Policymakers are left with a simple immutable fact set. The world’s nearly 8 billion people and $80 trillion economy is utterly dependent on hydrocarbons. Oil, natural gas, and coal together supply 85% of global energy, and oil itself supplies 99% of world transportation. The only prospects for meaningfully impacting those realities, and for forging new beneficial geopolitical outcomes, will be found in recognizing and capitalizing on the nature of these very real forces. It will be anchored in recognizing that America can sit at the table as an increasingly dominant player in these tenuous geopolitical times.

Former Secretary of Defense and former CIA Director Leon Panetta had it right when he said in 2015: “Too often foreign-policy debates in America focus on issues such as how much military power should be deployed …. Ignored is a powerful, nonlethal tool: America’s abundance of oil and natural gas.” The only modification to Secretary’s Panetta’s formulation I would suggest is changing the word “abundance” to “dominance.”

______________________

Mark P. Mills is a senior fellow at the Manhattan Institute and a faculty fellow at Northwestern University’s McCormick School of Engineering. Follow him on Twitter here.

- Kissinger, A World Restored, Oxford University Press, p. 258.

Are you interested in supporting the Manhattan Institute’s public-interest research and journalism? As a 501(c)(3) nonprofit, donations in support of MI and its scholars’ work are fully tax-deductible as provided by law (EIN #13-2912529).